Demystifying FATCA and CRS in under two minutes

Are you confused about FATCA and CRS? Here's a quick breakdown:

FATCA and CRS are two forms of Automatic Exchange of Information (AEOI). AEOI is an international standard for the automatic exchange of financial account information between tax authorities of different countries. It was developed by the Organization for Economic Cooperation and Development (OECD) and endorsed by the G20 countries to combat tax evasion by giving tax authorities access to information on foreign financial accounts held by their taxpayers.

FATCA, more completely, the Foreign Account Tax Compliance Act is originally a piece of US legislation that requires foreign financial institutions (FFIs) to report information on financial accounts held globally by US citizens and residents, to the US tax authorities.

CRS, more completely the Common Reporting Standard, is in many ways a global version of FATCA and requires financial institutions (FIs) to report information on accounts held by tax residents of Reportable Jurisdictions and certain entities controlled by such tax residents.

BVI and Cayman Islands implementation

The British Virgin Islands and the Cayman Islands, are both committed to the various international agreements. They were early adopters of both regimes and have implemented local legislation and regulations which mandate AEOI reporting on entities incorporated in the British Virgin Islands and the Cayman Islands.

Why is this important to me?

If you operate a BVI or Cayman Islands domiciled entity, it's crucial to understand your FATCA and CRS obligations. Depending on the classification status of your entity, you may have ongoing regulatory obligations. Non-compliance can result in legal and financial consequences.

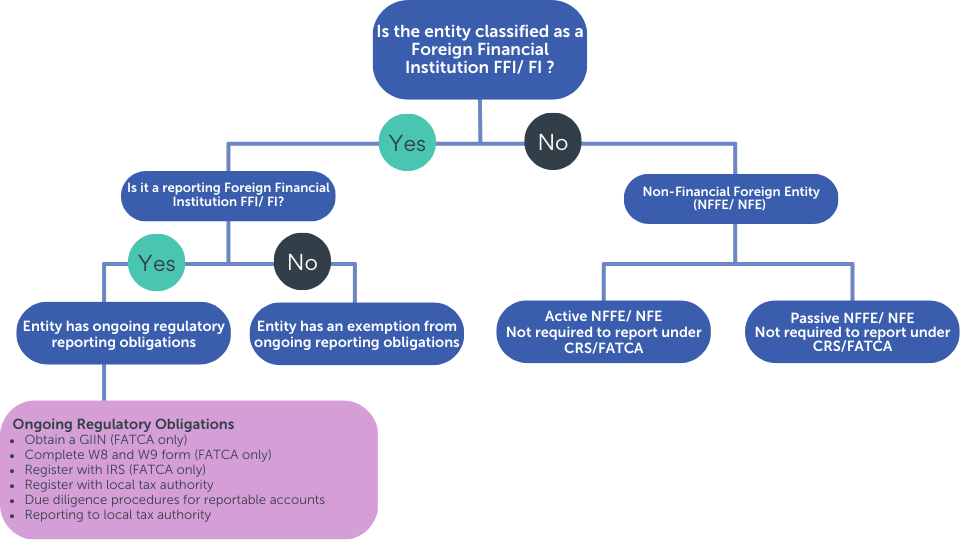

The diagram below shows a simplified overview of the different classification categories and their ongoing regulatory obligations.

FATCA/CRS classification decision tree

Under FATCA and CRS, entities fall into different categories that determine their regulatory obligations.

- Financial Institutions (FIs) under CRS or Foreign Financial Institutions (FFIs) under FATCA must comply with ongoing regulatory requirements.

- Meanwhile, Non-Financial Foreign Entities (NFFEs, under FATCA) or Non-Financial Entities (NFEs, under CRS) may have to self-certify their classification status when dealing with Reporting FFIs/FIs.

- Active NFFE/ NFEs do not have ongoing regulatory obligations, but may have to self-certify their classification status when dealing with Financial Institutions.

- Passive NFFE/ NFEs, on the other hand, must also self-certify their classification status when dealing with Reporting Financial Institutions, and may also be required to obtain self-certifications for the Controlling Person(s) of the entity.

Do you need help determining your entity’s classification status?

If you need help determining your entity's classification status, our Harneys CRS & FATCA Classification Solution can assist you. It's designed to make it easy for owners and directors of BVI and Cayman Islands entities to identify their regulatory obligations under both FATCA and CRS, and ensure compliance with these regimes.